London Mortgages Explained: How to Secure the Right Deal in Today’s Capital City Market

In Q1 2024, first-time buyers were responsible for about 72% of London home purchases, which shows how many people are trying to navigate London mortgages for the first time in a complex market. We are FEES FREE* Independent London Mortgages Advice Broker, and in this guide we explain how London mortgages work, how rates and property types vary by borough, and how our whole-of-market advice can help you choose the right option.

Key Takeaways

| Question | Key Answer |

|---|---|

| What is a London mortgage? | A London mortgage is a home loan tailored to the capital’s higher prices, varied property types, and specialist lending, often arranged through a local broker such as London Mortgage Shop. |

| How do I find the best mortgage rates in London? | You can review live rates on the dedicated London mortgage rates page, then speak to us for tailored, whole-of-market recommendations. |

| Can I get specialist advice by area? | Yes, we offer borough-focused guidance, for example for buyers in the City of London mortgage market and other central districts. |

| Is there expert help for prime central locations? | We provide bespoke lending advice in ultra prime areas such as Mayfair and Knightsbridge via our City of Westminster mortgage service. |

| Who can help with complex, high-value mortgages? | For properties in Kensington, Chelsea, Notting Hill and similar areas, our Kensington and Chelsea mortgage specialists arrange high-value and UHNW mortgages. |

| Is local knowledge important? | Yes, which is why we maintain borough-specific services, including our long-standing Camden mortgage and Islington mortgage advisory teams. |

| How do I speak to an adviser? | Call us on 0207 871 3023 for a FREE* adviser service and independent London mortgages advice. |

Understanding London Mortgages in Today’s Market

London mortgages operate in a market where average prices sit around £549,000, so loan sizes and affordability calculations are naturally more demanding than many other regions. Around 17.51% of UK mortgages were issued in London in 2023 to 2024, with the average London mortgage value at £266,822, which highlights both the scale and the intensity of activity here.

For buyers, homeowners and investors, this means you need a lender and product that match your income, deposit, and chosen borough. Our role as a FEES FREE* Independent London Mortgages Advice Broker is to interpret these conditions and secure the most suitable deal from across the whole market.

Why London Needs Specialist Mortgage Advice

Property in London ranges from Barbican leasehold flats and Islington townhouses to multi million pound mansions in Kensington and Belgravia. Each of these asset types comes with its own lending rules, valuation expectations, and risk considerations.

We work with lenders who understand specific London postcodes and construction types, so we can match you to underwriters who are familiar with local values, resale prospects, and tenant demand for buy to let cases.

Types of London Mortgages We Commonly Arrange

- First time buyer mortgages for flats and houses across Zones 1 to 6.

- Remortgages to secure better rates or release equity from rising values.

- Second mortgages and further advances for renovations or debt consolidation.

- Buy to let finance for investors in areas like Camden, Islington, and the City.

- Ultra high net worth (UHNW) and complex income mortgages in prime central London.

How London Mortgage Rates Work and What Affects Them

London mortgage rates are influenced by Bank of England base rates, lender funding costs, and individual risk factors such as loan to value and credit history. Because London loans are often larger, even small changes in rate can have a significant impact on your monthly payments.

You can keep an eye on the market by using our dedicated London Mortgage Rates resource, then we can help you interpret which of those rates you are realistically eligible for. We also review how long to fix your rate based on your budget, risk appetite, and plans for the property.

Key Factors That Shape Your London Mortgage Rate

- Loan to Value (LTV): Larger deposits usually secure lower rates.

- Property type and location: Some lenders price differently for flats, new builds, or ex local authority stock.

- Income structure: Bonus, commission, or self employed income can require specialist lenders.

- Credit profile: Strong credit histories open more competitive fixed and tracker products.

Why Local Rate Guidance Matters

In areas like Kensington and Chelsea, where typical first time buyer homes can cost around 5.9 times average earnings and mortgage payments of about £1,087 per month, structuring your borrowing correctly is critical. In contrast, some outer boroughs may offer lower entry prices but different lending policies around flats above shops or mixed use buildings.

We consider both the headline rate and the fees, incentives, and flexibility of each product, then explain the total cost over the initial deal period and full term in clear, simple terms.

First-Time Buyers and London Mortgages

London accounted for 12.8% of first time buyer mortgages in 2023, and in H1 2024 about 48% of London home purchases were by first time buyers, the highest share on record for that period. This shows a strong pipeline of new entrants who often need clear, patient guidance on borrowing, deposits, and realistic budgets.

As a FEES FREE* broker, we support first time buyers from initial affordability checks through to mortgage offers and completion, and we liaise with solicitors and estate agents to help keep your purchase on track. We can also explain available government or lender schemes where relevant, and how they interact with London prices.

Key Steps for First-Time Buyers in London

- Discuss your income, commitments, and savings so we can calculate a safe borrowing range.

- Obtain an Agreement in Principle to support offers on properties.

- Review mortgage options that suit your deposit and risk profile.

- Assess monthly payment comfort levels, including potential rate rises.

- Plan ahead for remortgage points when your initial deal ends.

Managing Expectations on Budget and Location

With London house prices flat in 2024 but still high in absolute terms, many first time buyers adjust their search areas or property types to align with lending capacity. Some choose emerging neighborhoods with better affordability, while others stretch to buy smaller but well connected central flats.

We help you compare options across multiple boroughs, explaining how local property values, service charges, and lease lengths can affect both your mortgage choice and long term financial plans.

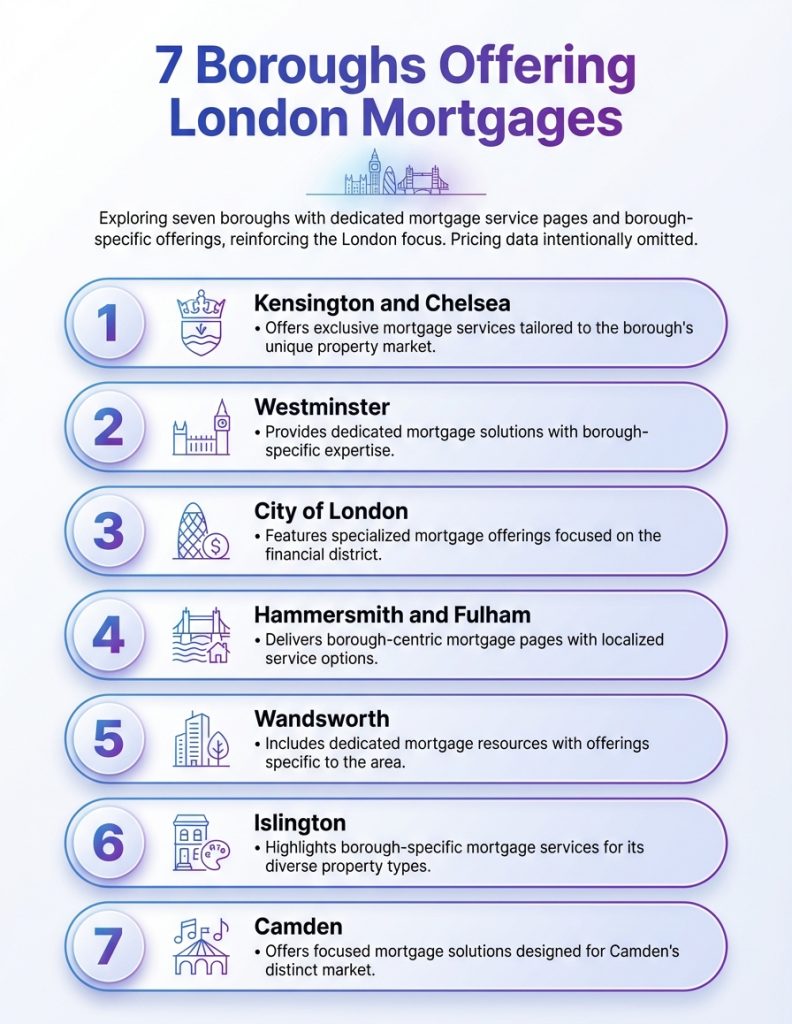

Seven London boroughs offering mortgages are highlighted. This infographic helps buyers compare options and terms across the capital.

Did You Know?

In H1 2024, 48% of London home purchases were by first-time buyers, the highest share on record for that period.

Remortgaging and Further Advances in London

Greater London remortgage balances averaged £265,937 in 2023 to 2024, which underlines how many homeowners here manage large existing loans. Remortgaging at the right time can reduce your rate, provide stability, or release equity for home improvements, investment, or other purposes.

We review your current deal, outstanding term, and any early repayment charges, then compare options from across the market to see whether switching makes financial sense. We also look at further advances and second mortgages if you want to raise additional funds while keeping your main deal in place.

Reasons London Homeowners Remortgage

- To avoid reverting to a higher standard variable rate when a fixed or tracker ends.

- To consolidate higher cost borrowing into a single, lower rate mortgage.

- To fund extensions, loft conversions, and other value enhancing works.

- To adjust the mortgage term and better align payments with retirement planning.

Remortgaging High-Value and Complex Properties

In districts like Moorgate, Cheapside, Kensington or Notting Hill, remortgaging can involve multi million pound loans and specialist underwriting. Lenders will often look closely at income diversity, company structures, and international assets.

Our experience with prime central London remortgages means we can present your case clearly, anticipating lender questions around bonus income, dividends, or non resident status where relevant.

Prime Central and Ultra-High-Net-Worth London Mortgages

Ultra prime locations such as Mayfair, St James’s, Knightsbridge, Belgravia, Chelsea, and parts of Kensington and Holland Park require bespoke lending. Mortgages here often exceed conventional maximum loan limits and rely on manual underwriting rather than standard scoring.

We work with lenders and private banks who understand UHNW client profiles, including complex income, significant investment portfolios, and multi jurisdictional assets. This allows us to negotiate terms that reflect your broader wealth position rather than salary alone.

Typical Features of UHNW London Mortgages

- Large loan sizes with flexible repayment structures and interest only options where appropriate.

- Consideration of global income and assets, not just UK employment.

- More nuanced views on property type, including listed or architect designed homes.

- Discreet, relationship based service across purchase, remortgage, and portfolio finance.

Why Specialist Support Matters in Prime Areas

In areas like Knightsbridge or South Kensington, standard high street criteria may not fit the property or borrower profile. We can introduce you to lenders who are comfortable with higher value flats, mansion blocks, and properties with unusual features.

We also help coordinate with your tax, legal, and wealth planning advisers so that borrowing sits comfortably within your wider financial strategy.

Borough-by-Borough: How London Mortgages Differ Across the City

One of the defining features of London mortgages is how much criteria and pricing can vary by borough and even by street. Lenders may view a Barbican leasehold differently from a Victorian terrace in Islington or a tower block in Southwark, even at similar price points.

Our borough specific services mean we can explain these nuances in plain language and guide you to lenders who are active in your chosen area. Below is a brief comparison of typical focuses in several central boroughs.

Example Borough Mortgage Focus

| Borough | Typical Focus | Common Property Types |

|---|---|---|

| City of London | Leasehold finance, remortgages on prime flats | Barbican estate, modern EC1 to EC4 apartments |

| City of Westminster | UHNW, complex income, high value purchases | Mayfair, Knightsbridge, Marylebone townhouses and flats |

| Kensington & Chelsea | Multi million pound loans, bespoke underwriting | Period houses, mansion blocks, mews properties |

| Camden | First time buyers, remortgages, buy to let | Terraced houses, ex local authority flats, conversions |

| Islington | Mixed professional buyers, portfolio landlords | Georgian and Victorian terraces, new build apartments |

Local Knowledge in Practice

In the City of London we secure finance for Barbican leaseholds, properties near Liverpool Street and Spitalfields, and remortgages in Moorgate and St Paul’s. In Westminster we handle bridging finance and other advanced lending in areas such as Pimlico and Victoria where chains and timescales can be tight.

In Camden, Hampstead, Belsize Park, and West Hampstead we have been arranging mortgages since the late 1980s, which helps when discussing local values, rental yields, and lender appetite for specific blocks or streets.

Did You Know?

Around 17.51% of UK mortgages were issued in London in 2023–24, with the average London mortgage value at £266,822.

Camden Mortgages: Diverse Stock and Strong Demand

The London Borough of Camden combines creative hubs like Camden Town with affluent Hampstead and Belsize Park, which creates a very mixed mortgage landscape. We have been providing independent access to the lowest and best rates for Camden residents since the late 1980s, giving us long term insight into the area.

Properties range from ex local authority flats to grand period houses, so lender criteria and valuations can vary street by street. We review lease terms, service charges, and construction types to ensure your mortgage is suitable and future resale continues to be viable.

Common Camden Mortgage Needs

- First time buyer loans for flats in Camden Town and Kentish Town.

- Remortgages and further advances for extensions in Hampstead and Belsize Park.

- Buy to let finance for student and professional lets near universities and transport hubs.

Camden as a Long-Term Investment

Many buyers in Camden are thinking about both lifestyle and long term capital growth. We help you model different mortgage terms and repayment strategies so your chosen product supports those goals.

For landlords, we examine rental income coverage requirements and stress testing to find lenders that align with your portfolio strategy and future borrowing needs.

Islington Mortgages: Townhouses, Conversions and New Builds

Islington covers neighborhoods such as Angel, Barnsbury, Canonbury, Highbury, and Finsbury Park, each with its own property character. Our comprehensive knowledge of the local market helps you secure a mortgage that is right for your specific street and building.

From Georgian terraces to modern flats, lenders will consider construction, conservation status, and lease details when deciding terms. We present this information clearly in your application so underwriters fully understand the quality and location of your home.

Buyer Profiles We Often See in Islington

- Young professionals purchasing first flats in Angel or Highbury.

- Families moving up to larger houses in Barnsbury or Canonbury.

- Investors purchasing flats around Finsbury Park for rental demand.

Balancing Budget and Lifestyle in Islington

Islington’s central location and amenities are attractive, but budgets must be carefully aligned to mortgage affordability. We compare fixed and variable products, explain overpayment options, and plan for future remortgages as your income and family situation change.

Because we are FEES FREE*, our focus remains firmly on long term suitability and clarity rather than product bias.

Outer London Boroughs: Space, Value and Different Criteria

Beyond Zones 1 and 2, areas such as Hounslow, Richmond, Kingston upon Thames, Merton, Wandsworth, and Ealing often provide more space per pound. Mortgage criteria can differ, particularly for houses with larger plots, mixed use streets, or properties near transport infrastructure.

We provide independent advice across these boroughs, considering school catchments, commuting patterns, and local regeneration plans that might influence future values. We also help existing owners remortgage or take further advances for loft conversions, side returns, and garden rooms.

Examples of Outer London Mortgage Considerations

- Assessing flood risk, building condition, and construction type in riverside areas like Richmond.

- Understanding lender appetite for maisonettes, ex local authority blocks, and flats above shops.

- Balancing borrowing between main residences and any buy to let properties you own.

Why Whole-of-Market Advice Helps Here

Some lenders are particularly active in outer London and commuter belt locations, while others focus heavily on central postcodes. As whole of market brokers we are not tied to a restricted panel, so we can select from a wide range of lenders depending on your exact situation.

This is important when you have nuanced needs, such as self employment, multiple incomes, or plans to move again in a few years.

How Our FEES FREE* Independent London Mortgages Advice Works

As a FEES FREE* Independent London Mortgages Advice Broker, our objective is to connect you with the most suitable mortgage for your circumstances, without charging you an advice fee in most standard cases. Instead, we are usually paid by the lender, and we always explain clearly how that works before you proceed.

We support clients across every London borough, from initial consultation to completion and beyond. Our advisers are available seven days a week, and you can speak to us on 0207 871 3023 to discuss your plans.

What You Can Expect When You Contact Us

- A detailed but straightforward conversation about your goals, budget, and timescale.

- Clear explanations of how much you can borrow and what monthly payments may look like.

- Whole of market comparisons of suitable mortgage products.

- Support with paperwork, valuation stages, and communication with solicitors and agents.

Why Clients Across London Choose Us

Our long history in areas like Camden, Islington, the City of London, and Westminster means we understand both the numbers and the local context. We combine this with up to date knowledge of mortgage criteria, regulatory requirements, and lender appetite.

Most importantly, our focus is on long term relationships rather than single transactions, so we aim to be the team you call each time you move, remortgage, or consider further borrowing secured on your London property.

Conclusion

London mortgages cover a wide spectrum, from first time buyer loans on starter flats to ultra high value arrangements in prime central districts, and each requires careful planning. With average loan sizes high, criteria detailed, and borough differences significant, working with a FEES FREE* Independent London Mortgages Advice Broker can save you time, stress, and potentially considerable money over the life of your loan.

Whether you are buying in the City, Westminster, Kensington and Chelsea, Camden, Islington, or any other London borough, we are here to help you understand your options and secure an appropriate deal. To discuss your situation with an experienced adviser, call us on 0207 871 3023 and we will guide you through your next steps in the London property market.